Like it or Not, Nvidia is still King.

Nvidia (NVDA) reported impressive earnings on Wednesday, August 28th, 2024, after the market closed, exceeding revenue and profit expectations for the second quarter. This strong performance is a testament to Nvidia's resilience and market position. Despite this, Nvidia shares experienced a decline after the release of their quarterly report, leading to some investor concern. Let's delve into the analysis to provide reassurance.

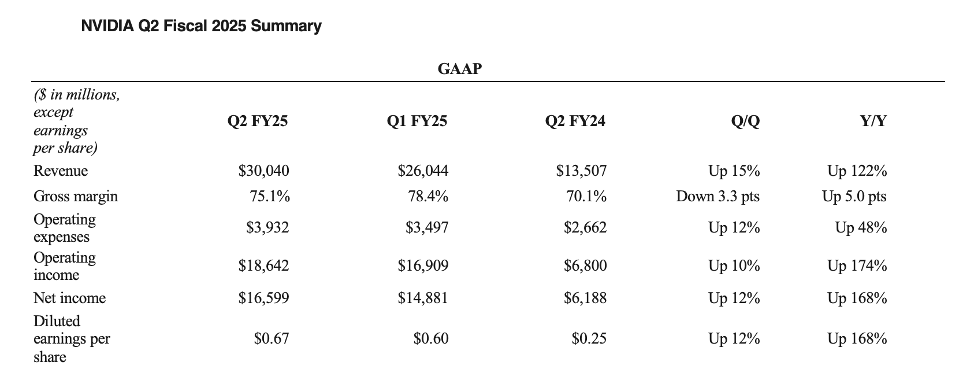

New Following the first quarter, the senior leadership team at Nvidia anticipated a Q2 revenue of $28 billion; however, they exceeded expectations by delivering $30 billion for the second quarter, reflecting a remarkable 122% growth compared to the previous year. The Gross Profit Margin stood at 75.1%, aligning with the anticipated range for Q2. One notable aspect was Nvidia's operating income, which reached $18.6 billion, reflecting a remarkable 174% increase. By calculating the ratio of Nvidia's operating income to its revenue, we can see that the company is achieving approximately 66% operating profit margins. Nvidia's operating revenue not only ranks among the industry's elite, but it also leads the pack. Both their revenue and operating income are experiencing remarkable growth of 100%. The Q2 results indicate that Nvidia is excelling across the board, with revenue, profits, and cash flow all on the rise. This performance resulted in an improved Q3 forecast of $32 billion, so what accounts for the decline in stock price despite the better-than-anticipated results?

Before delving into the reasons behind the price decline, it's important to highlight that the increasing efficiency of artificial intelligence fuels Nvidia's expansion. This development is generating a significant surge in demand from major players in cloud computing, such as Microsoft, Amazon, Alphabet, and Meta Platforms, all of whom are investing heavily in the construction of AI data centres. It highlights the pivotal role of Nvidia's Data Centre revenue in driving the company's growth. To emphasize this point, Nvidia's Chief Financial Officer Colette Kress noted that the robust sequential year-on-year growth was fueled by the demand for the Hopper GPU computing platform, which is essential for training and enhancing large language models, recommendation engines, and generative AI applications. She further noted that cloud service providers accounted for approximately 45% of Nvidia's data centre revenue, with over 50% coming from internet and enterprise computing companies. The 45% originates from Nvidia's leading four clients: Meta Platforms, Amazon, Alphabet, and Microsoft. The concentration has significantly increased, rising from 40% in the first quarter. Nvidia's CFO emphasized that acquiring their Hopper GPU is essential, as failing to do so would leave AI developers at a disadvantage. AI developers must embark on this journey, which is precisely why Hopper persists in its efforts. Her statement clarifies that while the hyperscalers are significant clients, the demand for Nvidia products surpasses supply, rendering the impact of the top four customers cutting back on their purchases negligible. It is important to note that this scenario is unlikely to change in the near future, providing Nvidia with a sense of business security from their top customers.

The drop in stock price is influenced by the impending launch of Nvidia's new chip - the Blackwell GPUs, which have been delayed due to changes being made to the Blackwell GPU mask intended to improve production yield; however, this modification led to a slower-than-expected ramp-up. Nvidia's CFO emphasized that the company had resolved the yield challenges associated with the Blackwell GPUs and was set to increase production in the last quarter of the year. She noted that Nvidia anticipates delivering 'several billion dollars in Blackwell revenue during Q4 2024 ', a significant projection that hints at the potential growth and future success of the company. 'We executed a change to the Blackwell GPU mass to improve production yields. Blackwell production ramp is scheduled to begin in the fourth quarter and continue into fiscal year 2026'.

The postponement of the official launch of the Blackwell GPUs is expected to impact both Q4 revenue and profit negatively. Nevertheless, Nvidia's senior management has assured us that Hopper GPUs will keep being shipped and sold, potentially offsetting revenue figures. Multiple sources suggest that the Blackwell GPU is expected to command a premium price, potentially leading to significantly increased profit margins for Nvidia stakeholders. This potential for increased profitability should instil a sense of optimism in our stakeholders. This statement is grounded in the confirmation from Jensen Huang, the CEO of Nvidia, during his appearance on Bloomberg Television on August 29, 2024, that the volume production of the Blackwell GPU will commence in Q4, leading to substantial revenues for Blackwell. He further indicated that the demand for Blackwell significantly surpasses its supply. Based on his assurances, it is anticipated that Nvidia is poised for a solid near and long-term outlook.

The delay of the Blackwell GPUs was a significant factor in the drop in Nvidia's stock. However, a more recent event on September 4th, reported by Bloomberg, has further impacted the stock. The U.S. Justice Department's decision to send subpoenas to Nvidia Corp and other firms as part of an investigation into potential antitrust law violations is a significant escalation. This news has once again put many investors in a state of panic.

Innovest Global Wealth found this noteworthy, as we have released numerous articles encouraging the inclusion of Nvidia stock in investment portfolios. Recently, the WSJ featured an article highlighting that Jensen Huang, the CEO of Nvidia, aims for the company to transform into a one-stop provider of data centres focused on the production and deployment of AI tools. This transformation not only aligns with the growing demand for AI tools but also opens up new opportunities for Nvidia. The potential of this transformation is significant, and it could pave the way for a promising future for the company. Understanding the implications of holding a substantial market share is essential. For instance, Nvidia's 80% market share in the chips powering artificial intelligence provides a level of flexibility. This dominance enables the company to dictate pricing strategies, whether that involves increasing or decreasing prices, due to the lack of substantial competition, as most rivals are either nonexistent or significantly lagging. This is illustrated by Nvidia's gross profit margin, which reflects its ethical approach to market pricing decisions, providing reassurance about the company's business practices. Another noteworthy aspect of holding a significant market share is that Nvidia is now encouraging customers to buy their additional offerings, such as CPUs, networking equipment, and more.

In summary, do you view Nvidia's influence as anti-competitive conduct? The reality is that Nvidia holds a distinctive advantage, commanding 80% of the market share, thanks to a product that significantly outpaces its rivals. Its dominance is evident, with demand far surpassing supply. Nvidia is leveraging its game-changing GPUs and influence in the market, and its transformation into a data centre provider is an exciting prospect for the future. Let us give the investigation a chance to prove us wrong.

We have written about numerous stocks, including Nvidia. Before investing, check our website to learn about their risks and how price fluctuations impact your portfolio.

Nvidia stock investors should be firm and weather the storms because Nvidia's future is getting brighter; like it or not, Nvidia is still king.

Take our Free IGW quiz below to receive your answers.

Take the Investment Risk Profile Quiz

This article is intended for informational purposes only. We strongly recommend that all investors conduct comprehensive research before considering any investment opportunity.

Contact Us

- UAE Office

Latifa Towers Trade Centre,

First Sheikh Zayed Road,

Dubai - United Arab Emirates

- Africa Office

Office 342, 4th Floor, The Acacia Mall, 14 - 18 Cooper Road Kampala - Uganda

+256 773 488 765

+254 721 287 135

info@innovestglobalwealth.com

Get In touch